EU–Mercosur 2026: What the Agreement Means for Germany and Agriculture – Opportunities, Risks, and a Realistic Look at “Sensitive” Agricultural Products

On January 17, 2026, the EU officially signed the EU–Mercosur package—consisting of a Partnership Agreement (EMPA) and an Interim Trade Agreement (iTA).

(policy.trade.ec.europa.eu)

At the end of February 2026, the European Commission also announced that it intends to provisionally apply key parts of the deal—a move that is meant to accelerate economic benefits, but remains highly controversial politically.

(apnews.com)

For Germany, the issue is highly relevant: On the one hand, export-driven sectors (mechanical engineering, chemicals, automotive) are hoping for improved market conditions. On the other hand, farmers and industry associations fear competitive pressure and “unequal standards.” This article provides a clear framework: What has been decided, what is still unresolved—and what does this mean in concrete terms for Germany, and especially for agriculture?

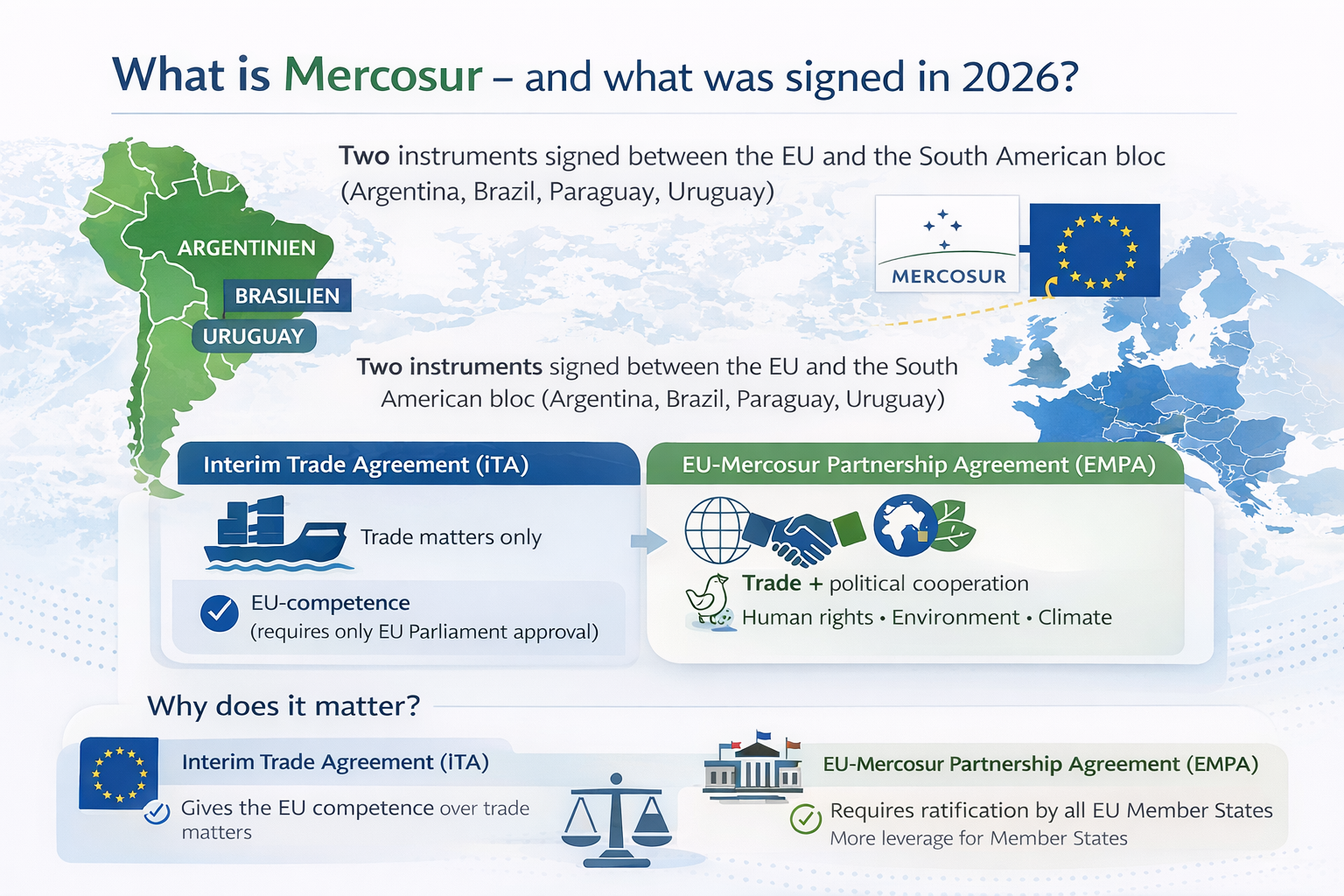

1) What is Mercosur—and what was signed in 2026?

Mercosur is a South American economic bloc (including Argentina, Brazil, Paraguay, Uruguay). From a legal perspective, the EU–Mercosur package is structured as two parallel instruments:

(policy.trade.ec.europa.eu)

- Interim Trade Agreement (iTA): covers trade matters only.

- EU–Mercosur Partnership Agreement (EMPA): additionally includes political cooperation (including human rights, environment, climate).

Important in practice: The iTA is considered EU-only (trade is an EU competence). It therefore does not require ratification by national parliaments of EU Member States—however, approval by the European Parliament remains necessary.

(bundesregierung.de)

The EMPA (the partnership pillar), by contrast, must be additionally ratified by the Member States.

(bundesregierung.de)

Why is “provisional application” so controversial?

On January 21, 2026, the European Parliament decided to ask the Court of Justice of the European Union (CJEU) to assess compatibility with the EU Treaties. As long as the Court’s opinion is pending, final approval is likely to be delayed (the EP think tank notes that more than a year is possible).

(epthinktank.eu)

Nonetheless, the Commission wants to put parts of the deal into effect provisionally—which critics describe as democratically problematic, while supporters view it as geopolitically and economically necessary.

(apnews.com)

2) What does the agreement mean for Germany overall?

Opportunities: market access, resilience, geopolitical diversification

Germany is among the clear supporters. In public debate, three main benefit logics are emphasized:

- Tariff reduction & market access

The BDI calls it an important success for the German and European economy and points to the EU’s capacity to act.

(bdi.eu) - Industrial and export effects

The VDA highlights that the automotive industry could benefit from reductions of high Mercosur tariffs (including on vehicles and parts) and that effects extend along European value chains.

(vda.de) - Geopolitics & supply chains

Supporters such as Germany and Spain also see the agreement as a lever to reduce dependencies and position the EU more strongly in global competition.

(reuters.com)

Risks: political polarization, legal uncertainty, acceptance problem

On the other side are (a) the legal and process debate (provisional application vs. parliamentary approval), (b) environmental and climate concerns, and (c) fears of unfair competition for EU farmers. These conflicts shape public perception—creating a corresponding risk for social acceptance.

(apnews.com)

3) Focus on agriculture: Why agri is so sensitive

In trade agreements, agriculture is almost always the toughest political issue—because it simultaneously touches food security, cultural identity, environment/climate, and incomes in rural areas.

That is why the EU–Mercosur package relies on a core instrument: tariff-rate quotas / tariff quotas (TRQs) plus safeguard clauses.

The core principle: “limited” access instead of full liberalization

For sensitive products, a high level of external protection remains—there is no simple “opening of the market.” Instead, imports are quota-limited and can be slowed if market disruptions occur. This logic is also emphasized by the Thünen Institute: sensitive products such as beef, poultry, and sugar remain protected; effects on production are assessed as rather small.

(literatur.thuenen.de)

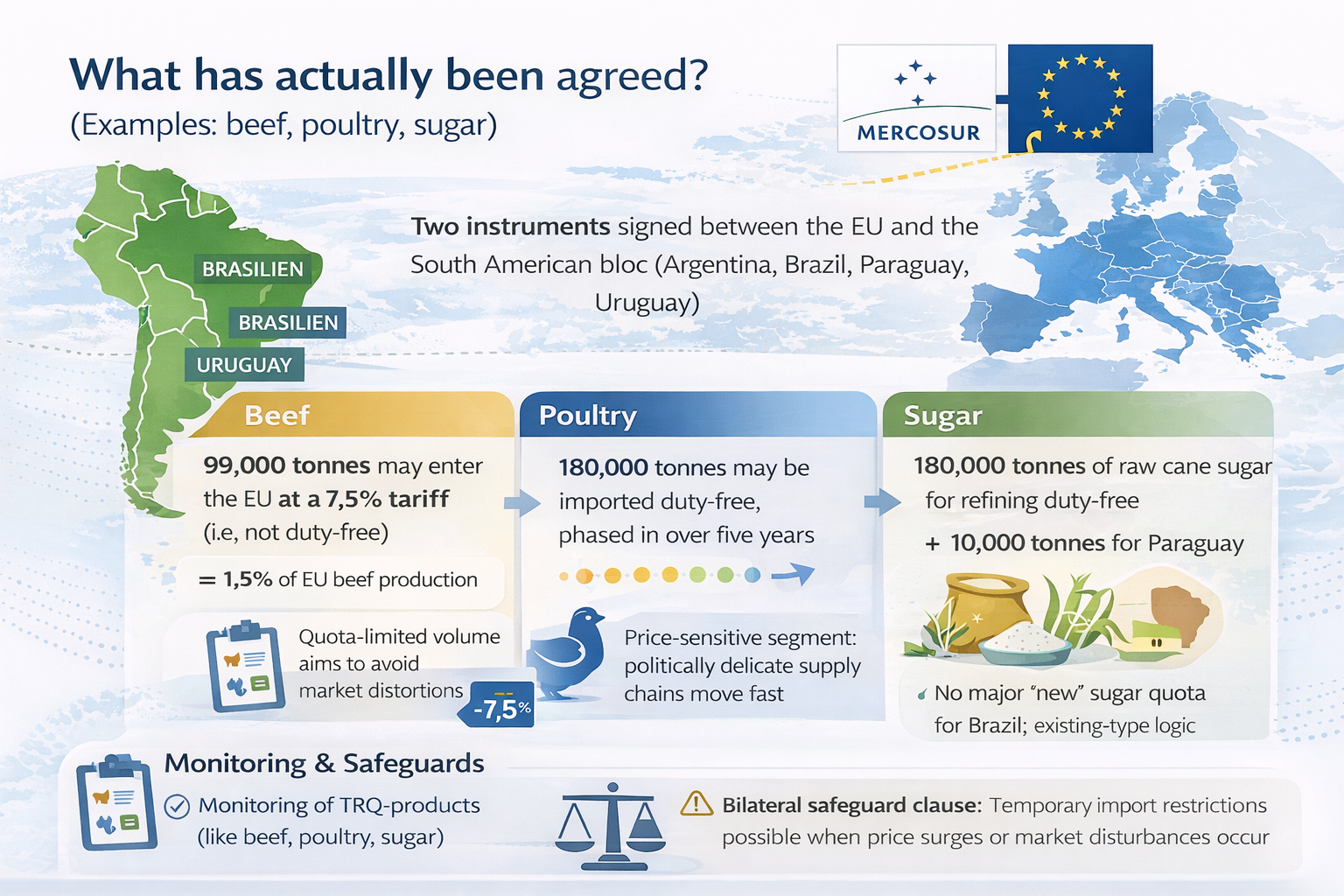

4) What has actually been agreed? (Examples: beef, poultry, sugar)

The European Commission has explicitly set out figures and mechanisms in a factsheet:

Beef

- 99,000 tonnes may enter the EU at a 7.5% tariff (i.e., not duty-free).

- The Commission frames this as a limited volume (about 1.5% of EU beef production).

Implications for Germany: The German beef market is part of an EU-wide market. Pressure is less about “volume alone” and more about segment overlap: if imported product competes strongly with certain qualities/cuts, it can be felt regionally—even at low percentage shares. The EU architecture aims to avoid a “shock” through quotas and protective mechanisms.

Poultry

- 180,000 tonnes of poultry may be imported duty-free, phased in over five years.

This is where a core of criticism lies: poultry is price-driven, supply chains move fast, and “unequal production requirements” (housing, animal welfare, antibiotics controls, environmental standards) are politically extremely sensitive.

Sugar

- No major “new” sugar quota for Brazil, but instead, among other elements, 180,000 tonnes of raw cane sugar for refining duty-free under an existing-type logic.

- In addition, 10,000 tonnes for Paraguay; specialty sugars excluded.

This matters because “sugar” is often portrayed in debates as a huge backdoor—while the details are far more technical.

5) Protection mechanisms: quotas are not everything—monitoring & safeguards are decisive

The EU side emphasizes two layers of protection:

1) Bilateral safeguard clause

If import surges or price disruptions threaten, the EU can adopt countermeasures—up to and including tariffs.

(consilium.europa.eu)

A relevant detail: according to the EU’s presentation, the safeguard clause can also cover imports under TRQs—this is politically an important signal to the farming sector.

(policy.trade.ec.europa.eu)

2) Enhanced monitoring for TRQ products

The Council explicitly references monitoring for products such as beef, poultry, pork, sugar, ethanol, etc.

(consilium.europa.eu)

In addition, the Commission mentions a €6.3 billion fund intended to counteract harmful effects in the “unlikely event” that they occur.

(policy.trade.ec.europa.eu)

6) What are the realistic pros and cons for German agriculture?

Potential disadvantages / risks (that should be taken seriously)

- Price pressure in sensitive segments (especially beef/poultry)—even if volumes are quota-limited.

(policy.trade.ec.europa.eu) - Competition via standards: if EU farms meet high requirements while imports can be produced more cheaply, an acceptance problem emerges. The German Farmers’ Association warns accordingly about negative market effects and competitive disadvantages.

(bauernverband.de) - Control and enforcement question: not “are standards written into the treaty?” but “do documentation, controls, and sanctions work in practice?”

Potential advantages / opportunities (often overlooked)

- Export opportunities for EU agri & food: the EU cites, among other things, facilitation and tariff reductions for products such as wine/spirits as well as dairy quotas (e.g., cheese 30,000 t).

(policy.trade.ec.europa.eu) - Protection of geographical indications (GIs): the EU references protection for 344 products (regional specialties) against imitation—relevant for premium strategies instead of volume competition.

(policy.trade.ec.europa.eu) - Resilience through diversification: the Thünen Institute also frames the agreement as contributing to trade diversification and crisis resilience.

(literatur.thuenen.de)

7) Unfounded fears—and justified questions

Three fears that are often exaggerated

- “Unlimited cheap imports”

This is not correct in such a blanket form: for sensitive products, quotas are foreseen; above them, higher tariffs apply; plus safeguard clauses.

(policy.trade.ec.europa.eu) - “The EU will drop its health and food safety standards”

The Commission is clear: EU SPS rules continue to apply—imports must comply as well.

(policy.trade.ec.europa.eu) - “The beef quota equals a major EU market shock”

The EU figure (99,000 t, 7.5% tariff) is large enough to debate—but it is not “the market will be flooded.”

(policy.trade.ec.europa.eu)

Three questions that are absolutely justified

- How robust are traceability and controls in reality?

- How will competitive disadvantages from EU requirements be compensated?

- How quickly do safeguards take effect in practice? (political speed vs. market speed)

8) What does all of this mean for consumers and companies in Germany?

For consumers, increased trade can, over the medium term, mean more choice and price effects in certain product categories—although agricultural prices in the EU are heavily influenced by global factors (energy, weather, feed, transport); the agreement is only one part of the picture.

For companies, the benefits are often more immediate: the BDI highlights tariff savings and market access; the VDA points to high Mercosur tariffs in the automotive sector and corresponding relief.

(bdi.eu)

9) Outlook: Why the deal also shifts attention to Brazil—right up to agricultural real estate

Precisely because trade and supply chains are being politically reconfigured, interest in Brazil as an economic region is growing—not only for industry, but also in the context of agriculture, raw materials, logistics, and infrastructure.

Anyone considering agricultural real estate in Brazil should, however, strictly separate two things:

- Trade agreement ≠ automatic land-price turbo

Prices are driven more by local factors (productivity, water, infrastructure, legal certainty, usage rights, climate risks) than by any single agreement. - Due diligence is essential

Particularly important are the chain of title, registry status, usage/water rights, environmental requirements, and land documentation.

Conclusion: What Germany truly needs now

The EU–Mercosur agreement is a geopolitical and economic milestone in 2026—but it comes with an acceptance problem that cannot simply be talked away. For Germany, opportunities lie primarily in industrial and export effects; for agriculture, what matters is whether quotas, monitoring, and safeguards function quickly and credibly in practice—and whether policymakers do not merely promise “fair standards,” but enforce them.

(consilium.europa.eu)